November 21, 2023

Power of Compounding!!

Let me start with simple principle we have always been taught since childhood. We should take proper diet regularly and timely that will provide us energy to work more effectively. But, when it is about savings, we always see common practice in many families is to spend our money first and invest with leftover amount. Is this the right analogy? May be not. We make sure we do 30-45 Minutes of regular exercise that keeps us fit. In the same way we should invest first and then spend what is left. This article is little long. I request you to read till end so it will make sense and help you in retiring early and fulfilling your Crorepati (Millionaire) dream.

What should be your mathematical equation to achieve your Crorepati dream. It is so simple!! “Income – Savings = Expense”.

I’m a Husband, Parent, Brother and I have gone through this rigor. My aim in this article is to help you get started and point you towards the right direction of savings and wealth creation for your family to fulfill above roles.

As a parent, it is quite natural if you have had those sleepless nights worrying about savings for your child to provide better education, secure life, quality living and avoid all the struggles you had when you were young.

The next question pops up, how much money is required by the time my child turns 18 for his higher education? How to generate so much money? How much to save, where to save and a chain of other related questions and worry how to accumulate such a huge money.

This seems as daunting as this may seen. Trust me; saving money efficiently depends upon disciple about regular investment. “Let us deal with discipline part first”.

If you think about ‘savings’ in terms of a mathematical expression, how will it look like?

Most likely you would say [Income – Expense = Savings].

Like many others, if you too think the above equation makes sense, then I’m afraid you’ve got it all wrong. If we go by the above equation, then we are essentially prioritizing expenditure over savings.

Agreed, expenditure over daily essentials is necessary, but many end-up spending a significant amount of money over lifestyle habits. Think about all the times you have bought that overpriced phone, or a fancy handbag, or camera, or sunglasses.

Each month the desire to own or experience something new and fancy slowly creeps in and we succumb. There is no harm doing this, after all, you are spending your own hard earned money.

The problem however is, it eats your ‘savings’ portion. This further leads to two serious problems –

- We save way lesser than what we are capable of saving and

- We save inconsistently.

So, how do we deal with this? Quite simple, we just need to rearrange the above equation

[Income – Savings = Expense]

The above rearranged equation appears very straightforward, but you will come to know the huge difference it makes by end of this article. By rearranging, we are essentially prioritizing savings over spending.

This literally means, the moment we draw our salary, first divert the funds towards savings and then spend whatever is left. This makes very big deal.

Adopting this approach is a way of life and requires a great amount of sacrifice and discipline, because you will have to live by the rules of this equation month on month, for many years. This, by no means, is an easy task. This implies that you cannot go out and pick up a fancy phone just because it looks fashionable in your hands. You are now forced to sacrifice this instant gratification for a bigger benefit which you would enjoy many years later.

The second important aspect is time. The sooner you start saving, the better it is for you and your family. In fact, I am always grateful who has advised me and I followed them and when I look back today, you cannot believe I am happily retired at age of 43. Yes, you read it right, I’m happily retired at 43.

What difference this makes, you may ask. Well, it makes a massive difference. Let me tell you a small story to help you understand the massive impact of time on savings.

A father gives his three young sons a lifelong pocket money of Rs.50,000/- each, every year. They are free to use this money in the way they decide. They are also given an option to invest this money in any legal instrument but with a condition that the investment made should not be touched till their 65th birthday.

Here is what each one does with their money –

● The elder one decides to save money very early in life. He started saving from his 20th birthday till 30th birthday (10 Years). He saved a total of Rs.5,00,000/-. After making his savings for 10 years, he enjoyed the remaining cash flow for the rest of life.

● The 2nd son enjoyed the cash flow first, but on his 28th birthday, he decides that he too needs to save the same amount as his elder Brother did. He saved money till his 40th birthday. The total savings was of Rs.6,00,000/-.

● The younger one also started saving his money from his 35th birthday onwards (After kids are grown up 4 and 6-year-old), but he decides to save all the money he receives until he turns 65. His total savings amounts to Rs.15,00,000/-

As mentioned earlier, investments grow at ‘very moderate’ rate of 12% year on year. Now, here is a question for you – can you take a guess on how much each person’s investment would grow to on their respective 65th birthday?

This may surprise you – how important role “power of compounding” has in our investments

● Elder son’s investment of Rs 5,00,000 grows to a whopping Rs > 5 crore.

● 2nd son who saved 6 Lakhs amount, his investment grows only to Rs 2.20 crore.

● The younger saved lot of money but he still cannot achieve what his both elder brothers achieved with their investments. His investment grows only to Rs 1.50 crore even though he saved more than his both brothers saved (11 Lakh vs 15 Lakhs).

Interesting right? Starting early in life makes a huge difference, so much so that the younger son’s massive investment of Rs. 15 lakhs (made over his lifetime) still cannot beat the elder one’s meagre investment of Rs. 5 lakhs made early on in life. As you may have realized, “Time” is making all the difference here. This is the “Power of Compounding”!

I’ve not been smart enough to make savings when I was 20 years old and I’m guessing not many who are reading this article would not have did this either. Given this, what do you think is our best option now?

Well, here is a bitter pill – we have to do what the younger son did if you are in Late 30s or go as per second son’s plan, if you are in early 30’s. As, we have not good as elder one’s investment strategy (you are lucky if you are in early 20’s then follow elder son’s principal), we need to increase our investment tenure and amount for more number of years.

To generate a significant amount of wealth for our families, we have to start saving continuously. I know these sounds like a long and boring plan, but well, there are no alternatives!

But here is a twist – the only thing that can compensate for lost time is higher ‘Rate of Return’. The higher rate of return can significantly compensate for the lost time. So, essentially, we should look at investing continuously in instruments which can yield a higher rate of return.

This leads us to the million-dollar question – where should we invest?

Before we get into that, let me tell you what most parents do in their pursuit of ‘saving for the child’. This, frankly, in my opinion, is a financial sin, please do not commit it.

Insurance/Insurance-linked ‘child’ plans

Run away from agents who try to peddle these insurance-linked savings plan for your child. Insurance is an expense and it cannot double up as an investment, whichever way you look at it.

Typically, these plans come with an annuity component, wherein a series of cash flow is expected when your child hits a certain age. The annuity component makes young, financially innocent, parents believe that the future cash flow would come handy when the child starts higher education.

However, if you break down the numbers you will realize that the rate of return on these instruments is mediocre, sub 6% in most of the cases. There are two serious problems with such ‘investments’; you not only commit large amounts of money every year (for many years) towards such low yielding avenues, but you also lose out on many attractive investment opportunities which can otherwise generate great returns.

Please avoid this and liberate yourself from such long, pointless financial commitment.

Savings Bank

Many parents open a bank account in the child’s name and start hoarding cash in the account. Cash in savings account creates an illusion of safety. In reality, money in a savings account is the probably the worst form of investment. Inflation is real and inflation will eventually vaporize your money’s purchasing power, and you won’t even realize this.

As you may know savings bank account yields are in range of 3.5 to 4% , the average inflation rate is about 5 to 6%, this means you are losing about 2% by parking your money idle in a savings bank account. A futile venture if you ask me.

So, what are the other investment options at your disposal? How should parents build a portfolio for their child? Well, here is what you can look at doing.

1. Equity-oriented Mutual Funds (50% to 60%)

I understand that many people find it scary to invest in a Mutual Fund. The usual thought is that mutual funds invest in stocks, and stocks are volatile therefore it is easy for one to lose money.

Yes, they are volatile and that is the nature of the beast. Imagine, if you had an option to see the valuation of your apartment on a daily basis. Naturally, the price of your apartment would vary (1Cr today, 95L tomorrow, 1.05Cr day after) – would you consider this volatile? May be not, as we believe real estate is the safest bet over the long term.

Likewise, investing in equities requires you to change your mindset. Stocks are volatile and the only antidote to volatility is time. If you give your mutual fund investment adequate time (which you should) then you can expect a great rate of return.

Historically, average returns of mutual funds over a 15 year period (in India) have been in excess of 14 to 15%, which as you can imagine is brilliant. Of course, there are funds which have delivered over 20% as well.

I’d strongly suggest you save up to 60% of your investable cash flow toward equity oriented mutual fund, via the SIP route. Most importantly, you need to give this investment time, at least 8 to 10 years in my opinion (Also let me give you simple formula to decide how much you should invest in Equity, if your age is 35, then 100-35 = 65, 65% should be in Equity and 35% in debt).

2. Fixed Income (30%)

By Fixed income, I’m not talking about the regular bank fixed deposits. You should explore options beyond this and venture into AAA rated corporate bonds. Some of the AAA bonds give you over 10% interest, which I think is great for a fixed income return.

Besides, an AAA rated bond implies there is a great amount of capital safety. Keep an eye out for these corporate bonds and consider investments in these instruments.

3. Gold (6-8%)

Don’t expect gold to deliver spectacular returns over the years. At best you can expect an average of about 6-8%. But you need this investment as a hedge against inflation. Gold to a large extent maintains the purchasing power of your money. Do not overexpose your investment in Gold, I’d advice not more than 10% allocation to gold (Personal Disclaimer I invest only 6%. Also, don’t buy physical gold, we should but Gold ETF or Gold Sovereign Units)

4. Index ETF (10%)

By definition, an exchange-traded fund (ETF) should just replicate the returns of its respective underlying. For example, an Index ETF like Nifty bee is supposed to mimic the performance of the Nifty 50 index. I think young parents should consider an exposure of at least 10% towards an Index ETF.

The rationale is very simple; an index like Nifty 50 represents the broad Indian economy. If you believe the economy will do good going forward, then naturally the index will also do well. If the index performs well, so will its ETF.

As you may have realized, the portfolio I’ve suggested is skewed towards equity. I personally believe that over the next few years, equity as an asset class will outperform every other asset class in India.

This is not a blind faith, but rather an outcome of a well-structured thought process. Perhaps discussing this thought process, itself will be another article, for another day. If you remember I said above I am happily retired at 43, by investing almost 70% of my savings in equity for last 15 years which gave me annual CAGR of 18%. But in this article, we have assumed only 12%. Imagine the value of portfolio if returns are 18%.Disclaimer: The author is founder of retireby49.com The views and investment tips expressed in this article are of his own and not that of the website or its management. Please talk to professional Financial Planner / Advisor for better financial planning.

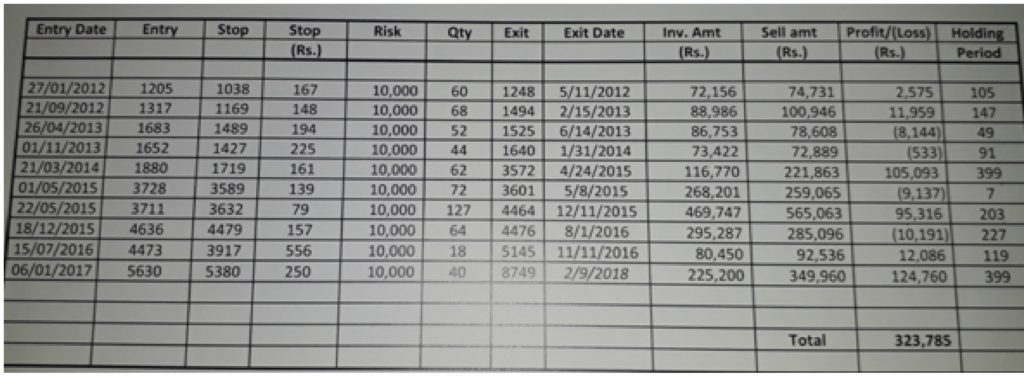

If anyone want to earn regular returns / build long term portfolio can use this strategy and we will be happy to help them.

If anyone want to earn regular returns / build long term portfolio can use this strategy and we will be happy to help them.